The United States federal debt continues to be one of the most closely watched economic issues as policymakers, investors, and households prepare for 2026. While government debt numbers may appear distant from everyday life, they can influence borrowing costs, interest rates, inflation expectations, and ultimately the monthly payments Americans make on mortgages and car loans.

Understanding the connection between federal debt and consumer borrowing can help households make smarter financial decisions in a changing economic environment.

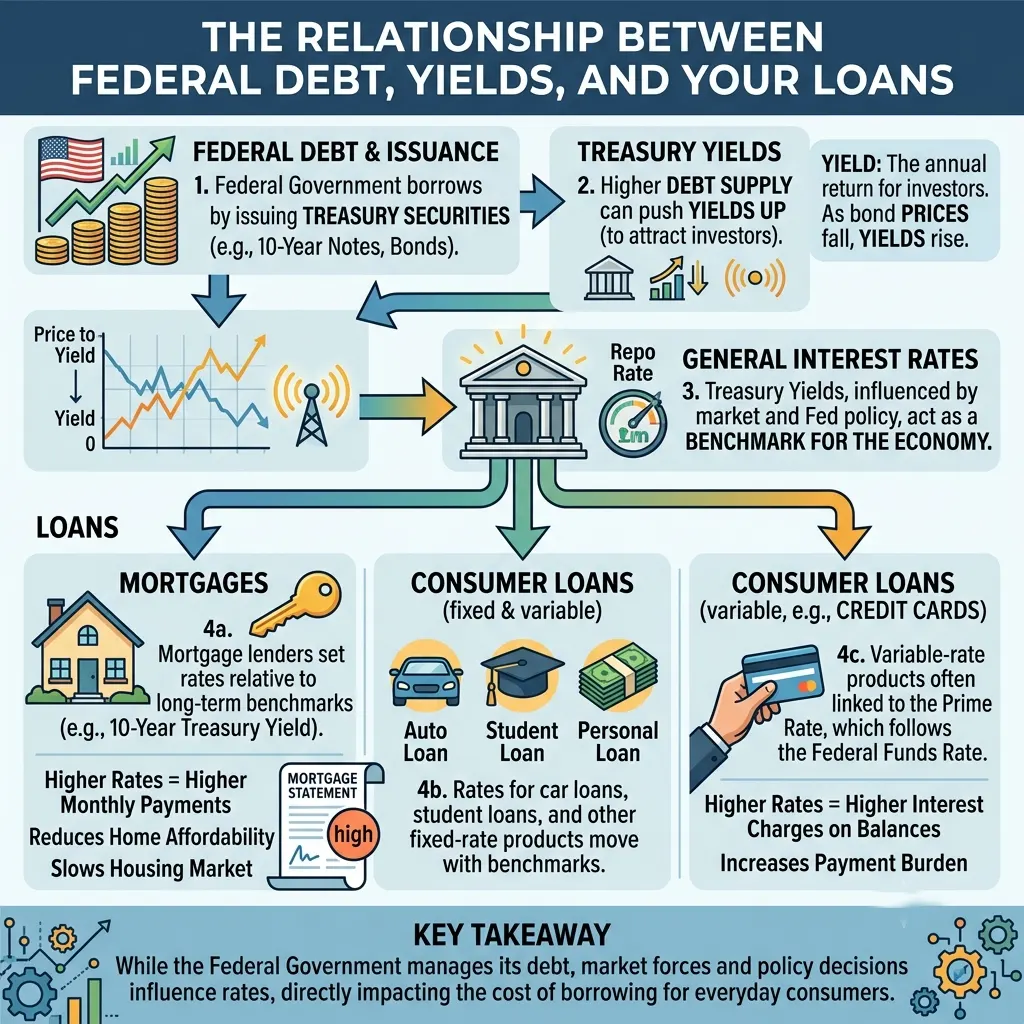

Why Federal Debt Matters to Everyday Borrowers

Federal debt represents the total amount of money the US government owes from years of borrowing to finance spending programs, investments, and public services.

According to information from the US Treasury Fiscal Data , government borrowing levels are closely monitored because they can influence financial markets and economic expectations.

Although federal debt does not directly set mortgage or auto loan rates, it can affect the broader financial environment where lenders determine borrowing costs.

How Federal Debt Can Influence Mortgage Rates

Mortgage rates are influenced by several factors, including inflation expectations, Federal Reserve policies, economic growth, and demand for government bonds.

When government borrowing increases, the Treasury may issue more bonds to finance spending. Changes in bond markets can affect long-term interest rates, which are closely connected to mortgage pricing.

Homebuyers should monitor:

- 30-year mortgage rate trends

- Federal Reserve interest rate decisions

- Inflation reports

- Housing market conditions

- Lender competition

The Federal Reserve provides updates on monetary policy decisions that influence borrowing conditions across the economy.

What Federal Debt Means for Car Loans

Auto loan rates are affected by similar economic forces. Higher market interest rates can increase financing costs for new and used vehicle buyers.

For example, a small increase in interest rates can significantly change the total amount paid over a five- or six-year car loan.

Consumers can reduce borrowing pressure by:

- Improving credit scores

- Comparing multiple lenders

- Making larger down payments

- Choosing affordable vehicle budgets

- Avoiding unnecessary long-term financing

Could Federal Debt Increase Inflation Pressure?

Economists continue to debate how government debt levels affect inflation. The relationship depends on factors such as economic growth, government spending, monetary policy, and investor confidence.

The Congressional Budget Office regularly analyzes federal budget trends and their potential economic effects.

The Role of Treasury Markets

Treasury bonds play an important role in global finance. They are considered a major benchmark for interest rates because many financial products are priced based on Treasury yields.

Information from the US Securities and Exchange Commission helps investors understand financial market structures and securities activity.

What Borrowers Should Watch in 2026

Consumers considering homes, vehicles, or refinancing should pay attention to several economic indicators:

- Federal Reserve rate announcements

- Inflation data

- Employment reports

- Treasury yield movements

- Bank lending conditions

Financial education resources from organizations such as Consumer Financial Protection Bureau can help consumers better understand loans and borrowing decisions.

Smart Financial Strategies for Higher-Rate Environments

If borrowing costs remain elevated, households can focus on financial preparation:

- Building emergency savings

- Reducing high-interest debt

- Maintaining strong credit profiles

- Comparing loan offers carefully

- Calculating total repayment costs

The US federal debt debate affects more than government budgets. It can influence financial markets, interest rates, and the cost of borrowing for millions of households.

While federal debt alone does not determine mortgage or car loan rates, understanding its relationship with the economy can help consumers make better financial decisions in 2026.

#USFederalDebt #MortgageRates #CarLoans #InterestRates #PersonalFinance #US Economy #FinanceNews #EconomicTrends #MoneyManagement