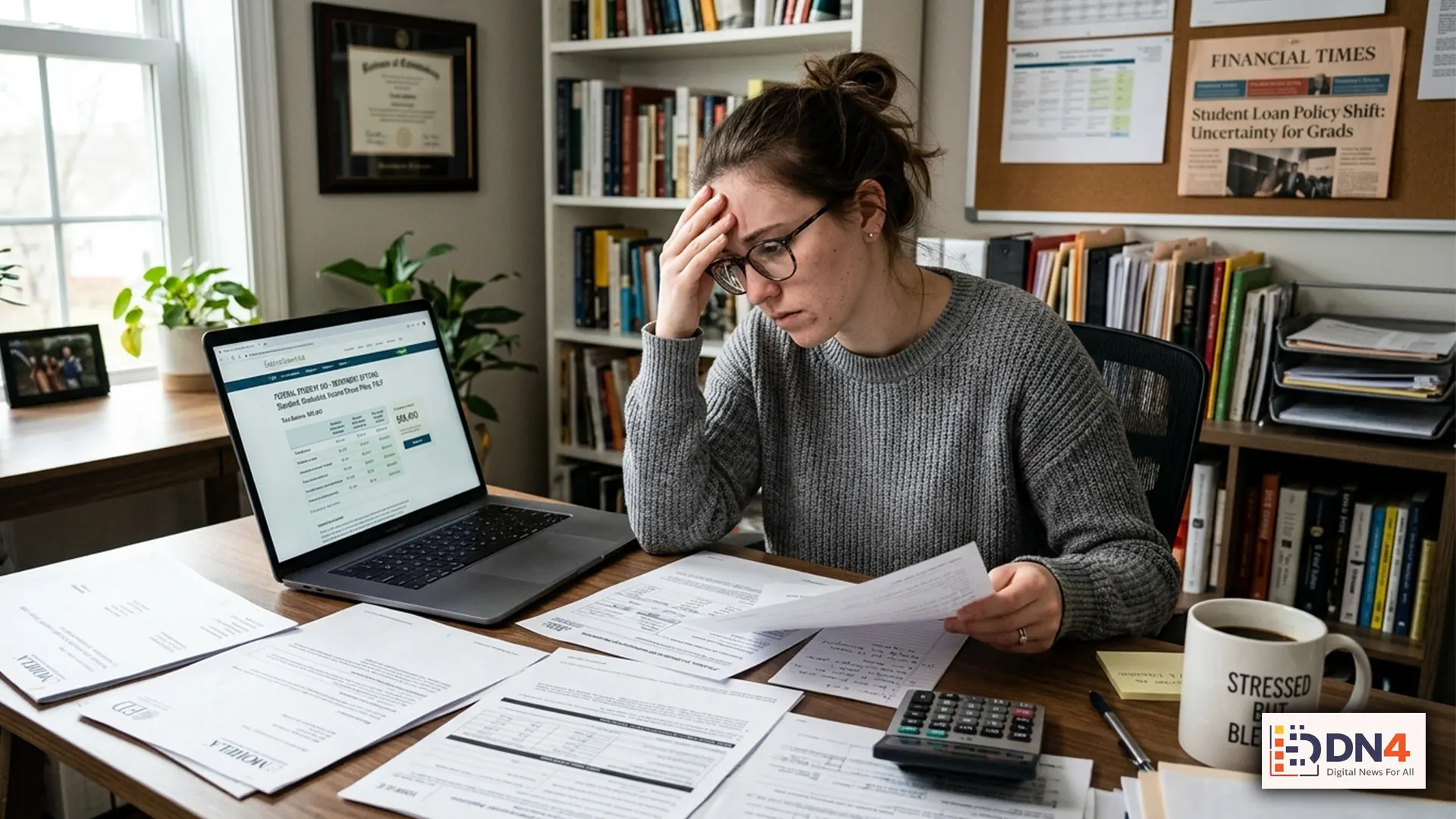

Millions of borrowers are once again being forced to rethink their repayment strategy as the U.S. Education Department rolls out another major student loan overhaul. If you’ve been confused by changes to the income-driven repayment system, uncertainty around the SAVE Plan, or new updates tied to repayment rules, you’re not alone.

The good news? If you act this month, you may be able to lower your payment, avoid unnecessary interest problems, or position yourself for future Public Service Loan Forgiveness.

What’s Actually Changing?

The latest policy moves are part of a broader federal effort to simplify student loan repayment and transition borrowers away from temporary pandemic-era confusion into more structured repayment programs. The Department has also proposed a new repayment framework that would begin affecting borrowers more directly in 2026, while some borrowers are already seeing account changes and repayment impacts now.

According to the U.S. Department of Education, officials expect a new repayment option called RAP to become available by July 1, 2026, while current borrowers should review their eligibility under existing plans now before more changes take effect.

Why This Matters for Your Wallet Right Now

If your monthly payment feels too high, this overhaul could create an opportunity to reduce it — but only if you check your options. Borrowers may still qualify for lower payments through Income-Driven Repayment (IDR), and in some cases, monthly bills can drop to $0 depending on income and family size.

Federal Student Aid servicer guidance also notes that borrowers can switch repayment plans and use the Loan Simulator to estimate lower monthly costs.

3 Smart Moves Borrowers Should Make This Month

1) Recheck Your Repayment Plan

If you’re still relying on an old repayment setup, you could be overpaying. The best move is to compare your current monthly bill with what you’d owe under Income-Based Repayment (IBR) or another IDR option.

2) Review Your Forgiveness Progress

If you’ve been paying for years, don’t assume the system is counting your progress correctly. Borrowers in qualifying plans may be working toward forgiveness after 20 to 25 years, while public service workers may be eligible sooner under PSLF.

3) Consider Consolidation Carefully

For borrowers juggling multiple federal loans, Direct Consolidation can simplify repayment. But it’s not always the cheapest move, so compare carefully before submitting anything. Some consolidation decisions can affect timelines, repayment eligibility, or future forgiveness strategy.

What About the SAVE Plan?

This is where many borrowers are still confused. The SAVE Plan has faced legal and administrative uncertainty, and official servicer updates indicate borrowers should continue checking for the latest status before assuming benefits or protections will remain unchanged. Some prior SAVE-related advantages have already shifted, including how interest treatment and future enrollment may work.

In plain English: if you’re on SAVE — or planned to enroll — you should not wait passively. Review your account, payment status, and backup repayment options this month.

The biggest mistake borrowers can make right now is doing nothing. The student loan system is changing again, and while the headlines are messy, the financial takeaway is simple: review your plan, estimate your new payment, and make sure you’re not paying more than you need to.

Even a small repayment adjustment today could save you hundreds — or even thousands — over time.

#StudentLoans #StudentDebt #LoanForgiveness #PSLF #IncomeDrivenRepayment #SAVEPlan #PersonalFinance #EducationNews #DebtRelief #MoneyTips #FederalLoans