This past week, global markets have been navigating a trifecta of powerful forces: fresh signals from the Federal Reserve, geopolitical tones from the G-7 summit, and a sharp swing in oil prices. Each development added new layers of complexity to an already uncertain macroeconomic landscape.

Fed Policy: Hawkish Pause with a Dovish Undertone?

The Federal Reserve held rates steady at its June meeting, as widely expected. However, Chair Jerome Powell’s tone during the press conference sent mixed signals to the markets. While inflation remains above the 2% target, Powell noted signs of cooling in labor markets and consumer spending, hinting that the Fed may be nearing the end of its tightening cycle.

Markets are now pricing in a cut as early as September, with futures suggesting a growing possibility of two cuts before year-end. Bond yields declined across the curve, and equities rallied modestly on the dovish interpretation.

Key takeaways:

- Fed funds rate held at 5.25–5.50%

- Powell acknowledges “balanced risks” between inflation and employment

- Core PCE still above target but showing signs of softening

G-7 Summit: Geopolitics and Economic Unity

World leaders convened in Italy for the G-7 summit, where the agenda was heavily shaped by two priorities: continued support for Ukraine and managing economic competition with China.

The group agreed on a plan to use frozen Russian assets to back a $50 billion loan for Ukraine—an unprecedented move that drew a sharp rebuke from Moscow. On the economic front, G-7 leaders emphasized “de-risking” from China rather than “decoupling,” signaling a more nuanced approach to trade and supply chains.

Markets reacted cautiously, with increased volatility in defense, commodities, and technology sectors—industries most exposed to global geopolitical shifts.

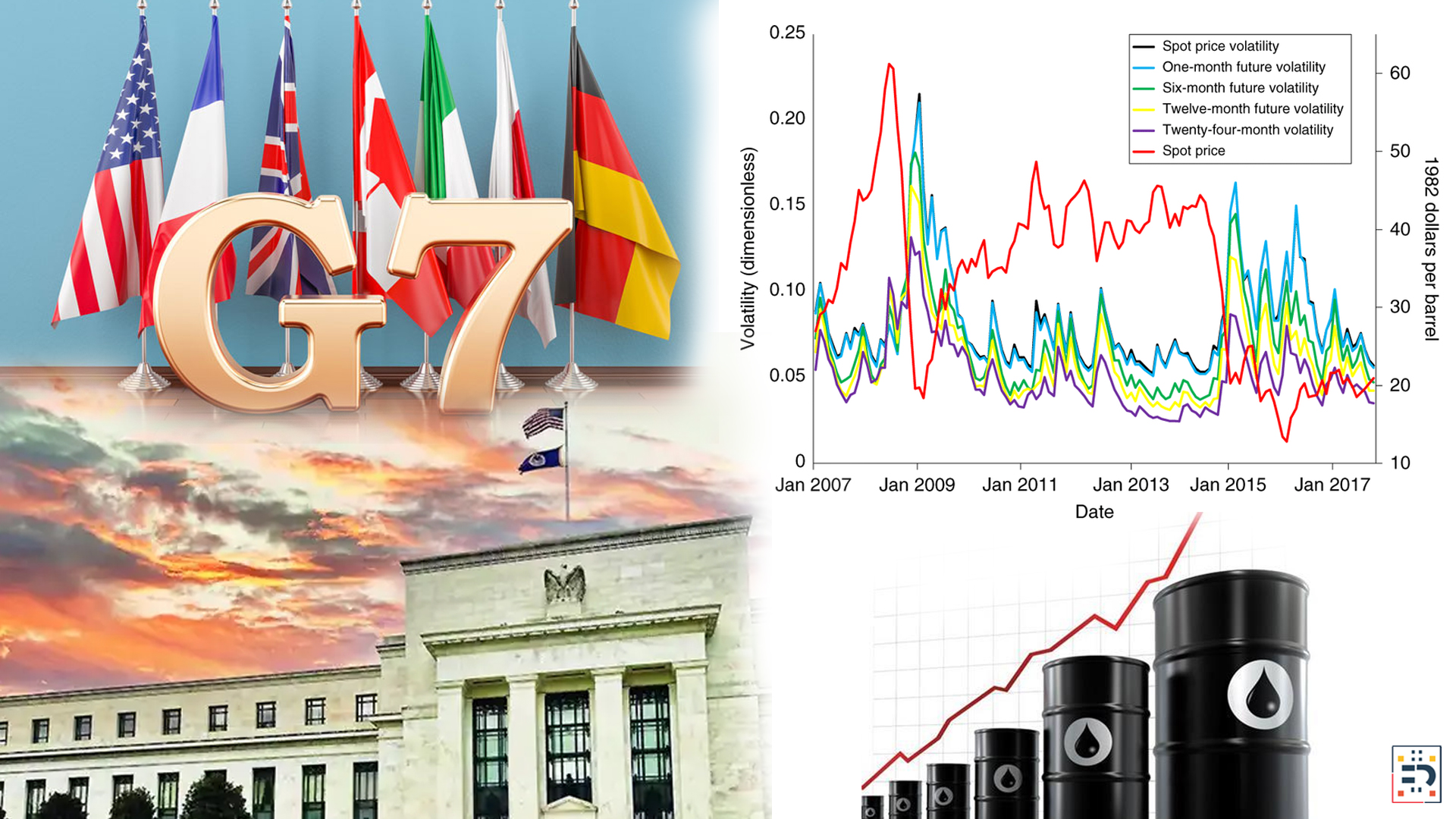

Oil Prices: From Supply Shock to Policy Shock

Volatility surged in oil markets after OPEC+ unexpectedly announced it would begin unwinding its voluntary production cuts by the end of Q3. Brent crude dropped over 6% in a two-day span, falling below $80/barrel before rebounding slightly.

The move raised questions about OPEC’s cohesion and the outlook for global demand. Analysts are now debating whether the cartel is betting on a soft landing for the global economy—or responding to internal pressure among member states.

Implications:

- Lower oil prices may ease inflation globally

- Energy stocks dipped, while airlines and transport rallied

- WTI and Brent volatility gauges spiked to their highest levels since March

Market Wrap-Up

Markets posted modest gains this week as investors digested a blend of dovish signals from the Federal Reserve and geopolitical tensions from the G-7 summit. The S&P 500 rose by 1.2%, buoyed by easing rate expectations and continued strength in large-cap tech. The Nasdaq outperformed, climbing 1.8%, with semiconductor and AI-related stocks leading the charge. In the bond market, the U.S. 10-year Treasury yield fell by 12 basis points, reflecting growing confidence that the Fed could begin cutting rates as early as this fall.

Meanwhile, Brent crude oil prices tumbled 4.5% over the week following OPEC+’s surprise announcement to unwind production cuts, causing sharp declines in energy stocks. On the flip side, transportation and airline sectors benefited from the prospect of lower fuel costs. Gold prices remained largely flat, as traders await clearer signals on inflation trends and central bank policy before making decisive moves.

Looking Ahead

Next week brings fresh inflation data from Europe, U.S. consumer confidence numbers, and earnings reports from major consumer and industrial firms. Markets will be watching closely to assess whether recent optimism is justified—or premature.