If your portfolio feels confusing in 2026, it’s because the economy isn’t moving in one clean direction.

It’s splitting.

On one side, a renewed oil shock — with crude flirting with $110 — is reviving inflation fears, pressuring consumers, and squeezing transportation, manufacturing, and rate-sensitive sectors. On the other, the AI-led compute boom continues to pour capital into semiconductors, cloud infrastructure, power systems, and data center expansion.

That disconnect is exactly why so many investors feel like they’re living through a K-shaped recovery: some assets are accelerating upward, while others are stuck in a higher-cost, slower-growth reality.

The result? Your winners and losers may no longer be separated by “growth vs value” or “tech vs non-tech.” Increasingly, the dividing line is this:

Who benefits from scarcity — and who pays for it?

To understand today’s market, you have to understand both sides of the split.

What Is a K-Shaped Recovery — and Why Does It Feel So Personal Now?

A K-shaped recovery happens when different parts of the economy recover at dramatically different speeds.

Instead of a broad-based rebound, you get two diverging paths:

- The upward leg: sectors, companies, and consumers benefiting from structural tailwinds

- The downward leg: those getting hit by inflation, debt costs, weak demand, or rising input prices

That framework became popular after the pandemic, but in 2026 it has taken on a sharper, more investable form.

This time, the split isn’t just about remote workers versus service labor or asset owners versus renters. It’s increasingly about:

- Energy producers vs energy consumers

- Compute suppliers vs compute buyers

- Capital-light software vs capital-heavy operators

- AI infrastructure winners vs margin-compressed laggards

In short: the market is rewarding leverage to scarce inputs and punishing exposure to rising costs.

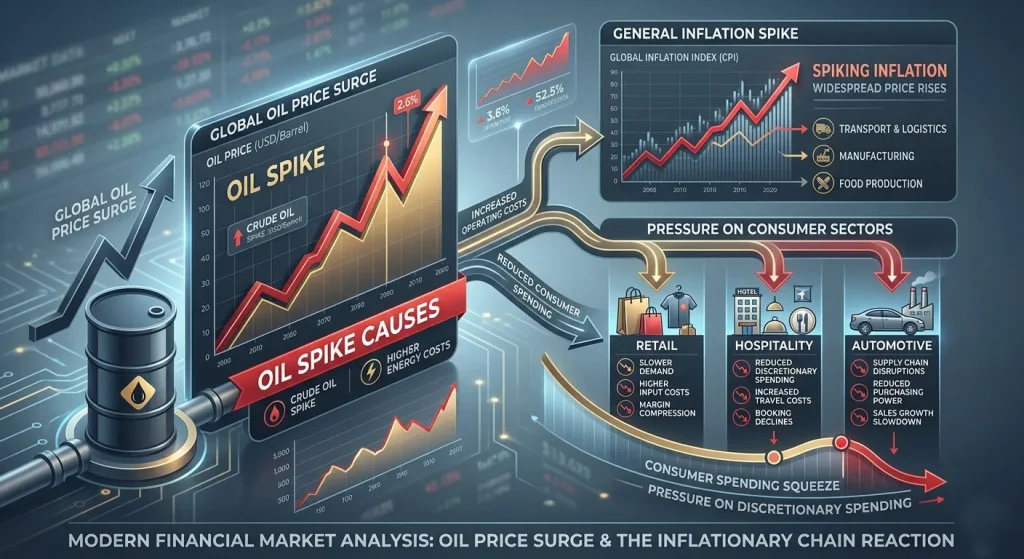

The First Shock: Why $110 Oil Changes Everything

Oil doesn’t just affect energy stocks. It acts like a tax on the entire economy.

When crude prices surge, the effects spread fast:

- Higher transport and logistics costs

- More expensive airline and freight operations

- Rising manufacturing input costs

- Pressure on consumer spending

- Sticky inflation that central banks can’t easily ignore

Investors often underestimate how quickly energy shocks ripple into broader portfolio performance. A move toward $110 oil doesn’t stay inside the commodity market — it leaks into earnings, margins, and interest rate expectations.

That’s why traders closely watch benchmarks and supply narratives from institutions and market trackers such as the U.S. Energy Information Administration, the International Energy Agency, and OPEC.

For portfolio construction, the message is simple: if oil remains elevated, parts of the market that depend on cheap energy and stable inflation assumptions become more fragile than they appear on paper.

The Other Shock: The Compute Boom Is Creating Its Own Winners

While oil squeezes the real economy, AI and compute demand are doing the opposite for a narrow but powerful set of industries.

The global race to build AI capability is driving spending into:

- Semiconductors and accelerators

- Cloud and hyperscale infrastructure

- Networking and memory systems

- Data center construction

- Cooling, power, and grid support

This is not just “tech optimism.” It’s capex reality.

Major investment themes now depend on who can supply the physical backbone of AI — not just who can build the next chatbot.

That’s why investors are paying close attention to trends in GPU infrastructure, AI productivity economics, and data center power demand.

The result is a market where one cluster of companies is being repriced for structural scarcity and long-duration demand, even while the rest of the economy struggles with higher costs.

Why Your Portfolio Feels Broken Even If the Index Looks Fine

This is one of the most frustrating parts of a K-shaped market: headline indices can look healthy while your actual holdings feel chaotic.

That happens because broad benchmarks can be carried by a relatively small set of winners, especially when AI infrastructure and mega-cap tech remain strong.

Meanwhile, large parts of the market may still be under pressure:

- Consumer discretionary names

- Industrials exposed to fuel costs

- Small caps with refinancing pressure

- Retail and lower-margin operators

- Capital-intensive businesses without pricing power

In practical terms, your portfolio may be experiencing two different economies at once:

- One portfolio bucket tied to scarcity, pricing power, and infrastructure demand

- Another bucket exposed to margin compression, inflation stickiness, and slower consumption

That’s the emotional reality of a K-shaped recovery: markets can be “up” while your diversification suddenly feels less protective than it used to.

The New Divide: Scarcity Assets vs Cost Victims

The easiest way to frame today’s market isn’t “bullish or bearish.” It’s this:

Scarcity Assets

- Energy producers

- AI chip and semiconductor suppliers

- Data center and compute infrastructure names

- Power and grid enablers

- Companies with strong pricing power

Cost Victims

- Fuel-sensitive transportation and logistics firms

- Margin-thin consumer businesses

- Capital-heavy firms with refinancing needs

- Operators dependent on cheap electricity or stable energy input costs

- Rate-sensitive growth names without earnings support

That framework matters because many investors still diversify using old playbooks that assume broad economic healing lifts most boats. In a K-shaped regime, that assumption breaks down.

Why the Compute Boom Doesn’t Cancel the Oil Shock

One of the biggest investor mistakes right now is assuming the AI boom can simply overpower macro pain.

It can’t — at least not evenly.

The compute boom is real, but it is also concentrated. It creates enormous value in specific parts of the market, while higher oil can still weaken broader economic conditions.

In fact, there’s a deeper twist here: AI itself is energy-hungry.

As model training, inference demand, and data center buildouts rise, the compute economy increasingly depends on power availability, grid resilience, and infrastructure spending. That means the boom is not floating above the physical economy — it is deeply tied to it.

That is why the next phase of market leadership may not just be “AI software” or “big tech.” It may include the less glamorous but highly investable backbone behind compute:

- Power management

- Industrial cooling

- Electrical equipment

- Energy transmission

- Physical infrastructure financing

What Investors Should Watch Next

If this K-shaped dynamic continues, investors should stop asking only, “Is the market expensive?” and start asking better questions:

- Which businesses can pass through rising costs?

- Which sectors benefit directly from capital spending on compute?

- Which companies depend on cheap fuel, cheap power, or easy refinancing?

- Where is scarcity creating durable pricing power?

- Which “growth” stories are actually infrastructure stories in disguise?

In 2026, macro investing is increasingly about identifying bottlenecks. Oil is one bottleneck. Compute is another.

And portfolios are being repriced accordingly.

How to Think About Positioning Without Overreacting

This isn’t a call for panic rotation. It’s a call for cleaner portfolio thinking.

In a K-shaped environment, investors may need to think in layers:

- Defensive exposure: resilience to inflation and energy shocks

- Structural growth exposure: AI, semis, data centers, and infrastructure

- Cost-sensitive exposure: positions that may need tighter scrutiny

- Cash flow quality: businesses that can absorb higher capital or operating costs

The point is not to chase whatever is hottest. It’s to understand why the market is rewarding some business models and punishing others.

Because once you see the split clearly, the market starts making more sense.

The $110 oil scare and the compute boom are not separate stories. They are two sides of the same investing reality.

One is tightening the old economy. The other is funding the new one.

That’s why your portfolio may feel both strong and fragile at the same time.

Welcome to the K-shaped recovery — where capital is still flowing, but not equally.

And for investors in 2026, the real question isn’t whether the economy is recovering.

It’s who gets to recover first.

#KShapedRecovery #OilCrisis #AIBoom #PortfolioStrategy #Investing2026 #AIInfrastructure #EnergyStocks #TechStocks #MacroInvesting