If you have not filed your taxes yet, this is the moment to stop doom-scrolling and start deduction-hunting.

The clock is ticking toward the April 15 tax deadline, and while most people assume their tax-saving opportunities are already gone, that is not always true. In fact, there are still a few deductions you may be able to claim right up until filing day — but only if you know where to look.

According to the IRS filing guidance, most taxpayers must file their federal return by April 15. And the IRS has also highlighted several deductions and filing tools that could reduce what you owe if you still qualify.

Here are 7 last-minute tax deductions that could still make a real difference before the deadline hits.

1) Traditional IRA Contributions

This is the classic last-minute move for a reason: it still works.

If you qualify, you may be able to make a Traditional IRA contribution for the prior tax year up until the filing deadline and deduct some or all of it, depending on your income, filing status, and whether you or your spouse had a workplace retirement plan.

It is one of the few tax-saving strategies that can still be funded after the calendar year ends — which is why it becomes deadline-week gold for procrastinators with cash on hand.

2) HSA Contributions

If you were covered by a qualifying high-deductible health plan, your Health Savings Account (HSA) may still be one of the smartest tax moves left on the board.

Under IRS HSA contribution rules, eligible taxpayers can generally make 2025 HSA contributions until April 15, 2026. For 2025, the IRS sets the HSA contribution limit at $4,300 for self-only coverage. Family coverage allows up to $8,550. Eligibility and catch-up rules may apply.

That makes the HSA one of the rare tax tools that can still lower taxable income even after New Year’s has come and gone.

3) Self-Employed Health Insurance Deduction

If you are self-employed, this one is easy to overlook — and surprisingly valuable.

The self-employed health insurance deduction may allow eligible taxpayers to deduct premiums paid for medical, dental, and qualified long-term care coverage for themselves, their spouse, dependents, and certain children.

The IRS explains in Publication 502 that this deduction generally applies if you had self-employment income and meet the plan and eligibility requirements.

Translation: if you paid for your own coverage and run your own business, do not assume those premiums are just financial pain with no tax upside.

4) Student Loan Interest

No, this one is not glamorous. Yes, it still matters.

Are you a teacher, counselor, principal, or classroom educator? If you paid for supplies out of pocket, do not leave that money behind.

According to IRS Publication 970, the deduction is subject to income phaseouts, and for 2025 it begins to phase out at higher modified adjusted gross income thresholds.

It will not erase your student debt trauma, but it may at least slightly reduce the tax sting.

5) Educator Expenses

If you are a teacher, counselor, principal, or classroom educator who paid for supplies out of pocket, this is your reminder not to leave that money behind.

The IRS has long allowed eligible educators to deduct certain unreimbursed classroom expenses, even if they do not itemize. That includes qualifying purchases like books, supplies, and other approved classroom materials.

This is one of those deductions people often “mean to claim” and then forget in the final rush. Which is tax season’s version of setting money on fire politely.

6) Charitable Donations (If You Itemize)

This one is less “last-minute” in the funding sense and more “last-minute” in the documentation sense.

Did you make qualified charitable donations during the tax year? If you plan to itemize, those gifts may still lower your taxable income. The IRS allows charitable gifts as itemized deductions. But there is a condition: your total itemized amount must exceed the standard deduction. See the IRS overview of itemized deductions and standard deduction rules.

The catch? If you cannot document it, do not count it.

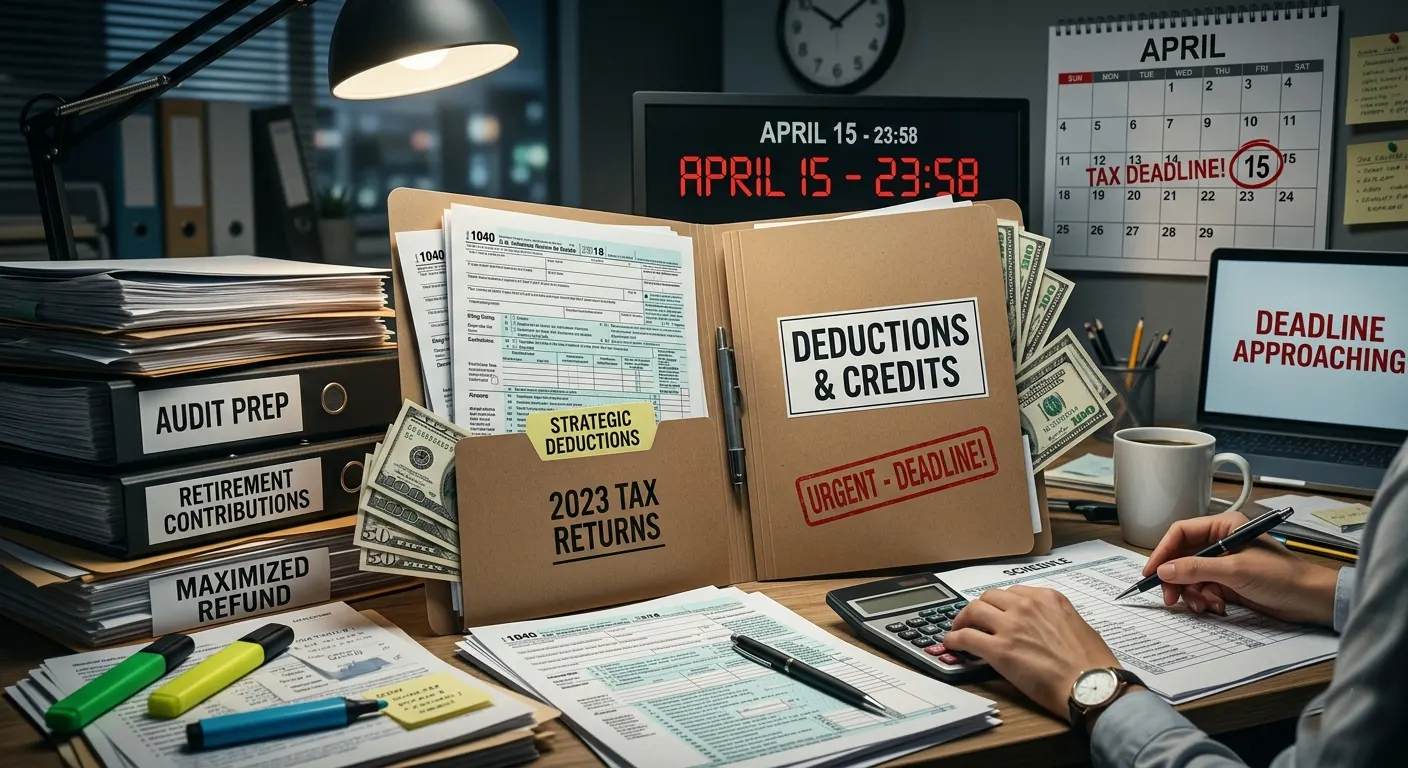

7) New 2025 Add-On Deductions Many Filers May Miss

Tax year 2025 brings several new or expanded deductions. Many taxpayers may not yet realize these exist.

The IRS says eligible filers may be able to claim new deductions tied to qualified tips, overtime, passenger vehicle loan interest, and an enhanced deduction for seniors using the new Schedule 1-A guidance.

This is exactly the kind of late-breaking tax detail that gets missed when people rush through filing software on autopilot.

If you have not filed yet, the worst move right now is assuming there is “nothing left to do.”

Some deductions disappear once the calendar flips. But others can still reduce your tax bill. IRA contributions, HSA contributions, and overlooked above-the-line deductions are key examples. Acting before the deadline keeps these options open.

Out of time to file cleanly? You can still request an extension to file. But note the distinction: the IRS does not grant an extension to pay taxes owed.

Because the only thing worse than overpaying taxes is overpaying taxes late.

#TaxDeductions #TaxDeadline #April15 #TaxTips #PersonalFinance #MoneyTips #IRS #TaxSeason #FinanceNews #SmartMoney #TaxFiling